Casablanca Stock Exchange: Facing Geopolitical Turmoil Mere market correction or cyclical downturn?

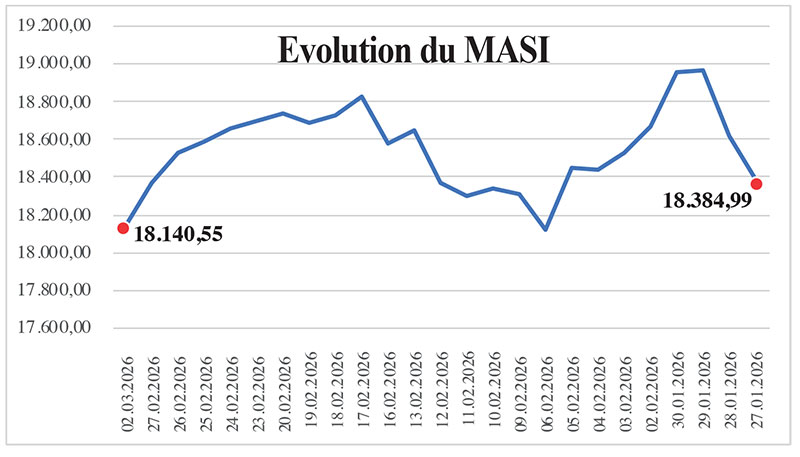

Monday, March 2 marked a psychological turning point for the Casablanca Stock Exchange. The Masi index fell 4.21% to 17,377 points, bringing its annual performance to -7.80%. The decline continued on Tuesday, March 3, with a 4.22% drop in the first half of the day. Beyond the magnitude of the movement, it is its nature that is striking: a corrective adjustment synchronized with the major global markets, triggered by renewed tensions in the Middle East and a sharp rise in risk aversion. The volumes, at MAD 1.15 billion (USD 123 million), are not insignificant. They were concentrated on the market’s blue-chip stocks, notably TGCC, SGTM, Itissalat Al-Maghrib, and Attijariwafa bank. This concentration reflects less a massive withdrawal of capital than a strategic repositioning on the most liquid stocks. In other words, investors reduced risk where they could do so quickly. The market correction in Casablanca is part of a global trend. In Paris, the CAC 40 index fell 2.17% on Monday, March 2. Frankfurt fell 2.6%, Milan 1.4% and London 1.2%. In the United States, the New York Stock Exchange held up better, limiting its decline to 0.1% at the close. The reaction of the financial markets to the air strikes in the Middle East remains relatively moderate at this stage. In this context, peripheral or mid-sized markets, such as Casablanca, tend to overreact, as their risk premium adjusts more quickly. Volatility is often amplified by more concentrated liquidity.

The key question is whether Casablanca’s reaction is proportionate to the risks involved. Fundamentally, the 2025 financial year confirmed the strength of the market. According to BMCE Capital Global Research, the overall turnover of listed companies grew by 9.9% to reach MAD 354.9 billion (USD 38.13 billion). Stocks of the industrial sector posted growth of 12.2% to MAD 230.5 billion, supported by the rise of mining company Managem, the momentum of construction groups such as TGCC and SGTM, and the expansion of the LabelVie network. Moroccan financial institutions, for their part, improved their net banking income by 5.4% to MAD 99.1 billion (USD 10.65 billion), driven in particular by Bank of Africa and BCP. Of the 67 companies that published their data, 55 posted annual revenue growth, reflecting a relatively widespread dynamic.

“These figures are difficult to reconcile with the idea of a structural weakening of the listed market. Especially since the market has benefited from renewed interest over the past two years, as evidenced by several IPOs, a gradual return of retail investors, and preparations for the launch of the futures market ”, notes a trader who is active in the market. The institutional base has consolidated and market depth has improved, even though liquidity remains concentrated on a limited number of large caps.o

Fédoua Tounassi