Finance Bill /Minimum Contribution: The minimum wage is putting up resistance

The minimum tax that all taxpayers subject to the Corporate tax or to the Income tax must pay even in the absence of profits still has a bright future ahead of it. «Among other proposals, we tabled an amendment to reduce the rate as provided for in the framework law adopted after the 3rd Taxation Conference, which provided for a minimum contribution of 0%.

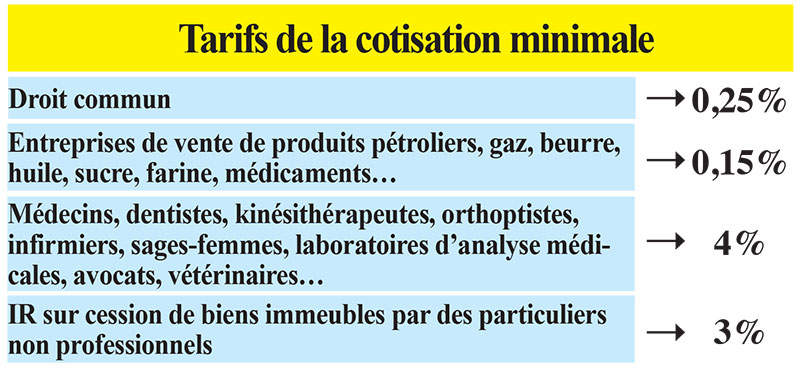

Although it did fall from 0.5% to 0.25% and 0.15% for certain sectors, the minister did not accept the amendment because of its impact of nearly MAD 1 billion (USD 108 million) on tax revenues. He did, however, commit to reviewing it next year in light of revenue trends», explained Youssef Alaoui, president of the CGEM employers’ parliamentary group in the second chamber of Parliament.

The recommendations of the 3rd Taxation Conference, held on May 03 and 04, 2019, as published online by the Ministry of Finance, provided for «gradually restructuring the rules for calculating the minimum contribution with a view to its abolition by 2024». These recommendations were not included in Framework Law No. 69-19 on tax reform.

It should be noted that the piece of legislation refers only to a gradual reduction in rates. Thus, rather than being abolished outright, the scale has been revised in recent years to stabilize at 0.25% and 0.15% depending on the sector. «The reduction has indeed begun. We are not there yet, but we are hopeful that it will be completed in 2027 or 2028» , added Youssef Alaoui. The CGEM parliamentary group had proposed, as part of the Finance Bill, to reduce the standard rate of the minimum contribution from 0.25% to 0.15% in accordance with the provisions of the Framework Law on Tax Reform.

This proposed amendment was rejected and could perhaps be considered for the 2027 Finance Bill. «This option is like trying to square the circle, because many companies only pay the minimum contribution» , warned a tax expert.In the meantime, the taxpayers concerned will continue to pay the minimum tax according to the scale in force at least for the 2024 and 2025 financial years until its repeal. «This is not normal and it is unconstitutional, because it amounts to taxing loss-making companies, which should instead be helped. The pretext is the fight against false losses, which should be monitored and penalized instead of penalizing everyone», says a certified public accountant.

The minimum tax on turnover was introduced by the 1987 Finance Act, inspired by the French annual flat-rate tax (IFA), which was created in 1973. At the time, rates were set between 0.30% and 0.75%. The principle is to encourage taxpayers to contribute in some small way to the financing of the general State budget and to fund public services and infrastructure development.o

Hassan EL ARIF