Local taxation: The Ministry of the Interior is no longer taking any chances with the TNB

Many property owners have recently been surprised to receive, for the first time in a long while, a tax bill for the Undeveloped Urban Land Tax (TNB).

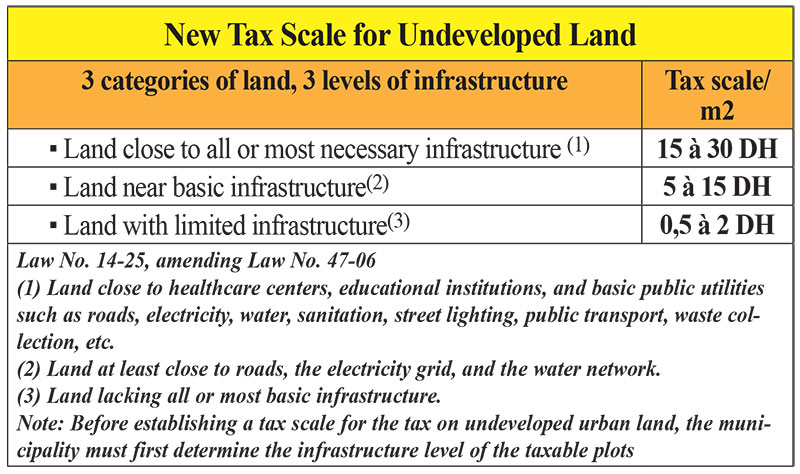

Before establishing a tax scale for undeveloped land in urban areas, the municipality must first determine the level of infrastructure on the taxable land.

A growing number of municipalities are contacting taxpayers and collecting this local tax, which falls within their mandate. However, many others are still dragging their feet, depriving them of a valuable source of revenue. Consequently, the Minister of the Interior has just sent a circular to the walis (head governors) and to the governors, clarifying that, despite the clarity of Law No. 14-25, amending Law No. 47-06 on local taxation, the application of its provisions varies from one municipality to another, particularly regarding the determination of the tax rates for undeveloped land, which is one of the new features of the law. Municipalities are therefore required to establish a new tax scale based on the level of infrastructure on undeveloped land located in urban areas or in rural municipalities with an urban development plan, in accordance with the scale stipulated by law. Governors and other local authorities are instructed to ensure that the conditions are already met to apply the National Land Tax (TNB) to undeveloped land within their jurisdiction. In this regard, it should be noted that some municipalities are levying taxes by conflating land with development plans and land covered by an urban planning document, even though the latter should not be subject to the TNB.

The circular from the Interior Ministry also insists on the activation of the commissions provided for in Article 42 of the law and composed of representatives of urban agencies, the prefecture or province, the municipality and regional multi-service companies (SRM).

Municipalities must also implement final court decisions regarding exemptions from the TNB (Taxe sur les Propriétés Bâties – Property Tax on Built Properties). Furthermore, the majority of municipalities apply the full rate, while the supervisory authority advocates for progressive taxation. The Interior Ministry’s guidelines on the TNB aim to ensure tax fairness within local communities and to take into account taxpayers’ financial means.

The TNB scale is defined by the council of the municipality concerned for the districts, sectors and villages according to their category and can vary as long as it takes into account the threshold and ceiling of the scale as defined by law.o

Hassan EL ARIF