Payment deadlines: Are you ready?

In contrast to the self-reporting nature of taxes, duties, and fees, the Directorate General of Taxes (DGI) holds exclusive authority to conduct audits. The same applies to provisions regarding payment deadlines. The affected businesses have received the first audit notices concerning VAT, corporate income tax, individual income tax, and the Social Solidarity Contribution, along with the payment deadlines. While the former are governed by Articles 210 and 212 of the General Tax Code (CGI), the procedure for auditing payment deadlines is codified by Article 78-7 of Law No. 69-21 and detailed in a circular published by the DGI.

Pursuant to said law and the delegation of powers by the Ministry of Finance, the tax administration is authorized to verify the accuracy and truthfulness of the information provided in the periodic returns required by Article 78-4 of the law.

The procedures for such audits have been modeled almost entirely on those applicable to taxes, duties, and fees. Indeed, when the tax authority decides to audit a business regarding payment deadlines, it sends the business a notice at least 15 days in advance of the audit’s start date. It should be noted that this audit will take place on-site at the company’s premises and that the law does not provide for documentary audits. It will be carried out by sworn agents of the General Directorate of Taxes (DGI), depending on the circumstances, at the company’s registered office, tax domicile, or principal establishment.

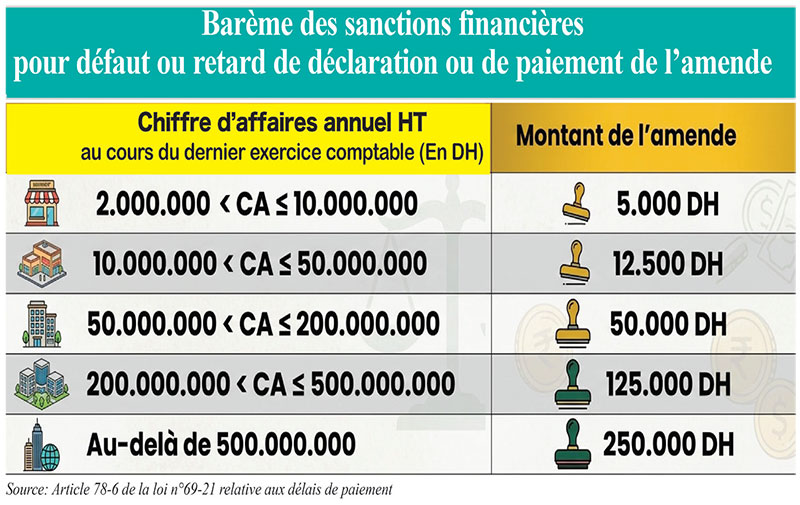

During the verification process, the individuals concerned are required to provide all necessary documents or supporting evidence. Failure to do so will result in notification of the penalty stipulated in the first paragraph of Article 78-6 of the law concerning payment deadlines. Financial penalties ranging from 5,000 Dirhams (USD 534) to 250,000 Dirhams (USD 26,678) , depending on the company’s turnover, are applicable for failure to file or delay in filing the periodic declaration or paying the corresponding fine.

The violations observed by the inspector are recorded in a report, a copy of which is given to the person concerned. From that date, the person has 30 days to submit their observations. If there is no response, an insufficient or unfounded response, or a response submitted after the deadline, the penalties due for the observed violations will be issued by order of revenue.

Hassan EL ARIF